On 20 January 2026, the UK Government proposed sweeping reforms to the UK mergers and markets regime as part of its continued drive for economic growth and its goal for the UK to operate a “best‑in‑class” competition regime. The reforms are set to radically overhaul the decision‑making process for in‑depth investigations and tighten some of the CMA’s key jurisdictional tools for mergers intervention, not long after the procedural changes announced by the CMA last year following growing criticism of over‑intervention.

While the reforms will improve predictability and transparency in some areas, the headline move – abolishing the CMA’s independent Phase 2 “panel” process – raises concerns around CMA accountability in the absence of a stronger appeal standard, and prompts a fundamental question: why is such radical shift change needed when CMA interventions have fallen so sharply in the past year? The consultation is now open and closes on 31 March 2026 – we would be happy to assist with any planned response strategy.

Key Takeaways

-

The CMA’s “panel” decision-making process for in-depth investigations will be replaced with newly created sub-committees of the CMA Board made up of senior CMA executives, non-executive directors and a new group of non-CMA staff experts, modelled off the UK’s recently introduced digital markets regime.

-

Changes to further tighten the CMA’s key jurisdictional thresholds of “material influence” and “share of supply” will be hardwired into legislation, with flexibility for the Government to make amendments if “significant competition challenges” arise in the future.

-

The two-stage UK markets regime will be collapsed into a single-phase review tool typically lasting 6 to 12 months, with greater flexibility over the prioritisation of concurrent investigations by sectoral regulators as well as more regular reviews of market remedies at least once every ten years and greater use of “sunset clauses”.

-

A single test will be created for the markets regime, focused on whether features of the market have an adverse effect on consumers (this is currently the test for market studies only; in-depth market investigations consider whether there is an adverse effect on competition).

-

The CMA will also have stronger powers to investigate algorithms across its competition and consumer protection responsibilities by issuing information notices, and the Secretary of State will have a formal role in a wider range of key guidance documents.

-

The CMA’s consultation on its proposed reforms is open until 31 March 2026, with most major changes – including those above – not likely to come into force until the end of this year at the earliest following completion of the legislative process.

Abolishing the “Independent Panel” for In-Depth Merger and Markets Investigations

-

In a radical overhaul, the Government has announced plans to abolish the long-standing “panel” of independent decision-makers for in-depth merger investigations and the new single-phase market review tool – an institutional feature of UK competition law since 1948 – and replace it with new sub-committees of the CMA Board appointed by a Mergers Board Committee and Markets Board Committee. Modelled on the digital markets regime, the sub-committees are expected to comprise senior CMA executives, non-executive directors as well as a pool of external experts appointed by the Secretary of State for Business and Trade, with the CMA Chief Executive, Sarah Cardell, sitting on panels for the most significant cases. Notably, the Government is not proposing to require sub-committees to include at least two non-executive directors of the Board (or one where the Chair is also a member) such as in the digital markets regime to draw more flexibly on a pool of non-CMA staff experts.

-

This proposed change is significant. The reform is intended to address accountability concerns arising from CMA leadership presiding over final panel decisions without direct input, and to allow closer alignment between case outcomes and wider CMA objectives, including those set out in its 2026–2028 strategy and the Government’s Strategic Steers. In practice, this could enable policy approaches adopted at Phase 1 – such as the CMA’s recent “step back” approach in global mergers – to shape the scope of Phase 2 investigations or the design of remedies.

-

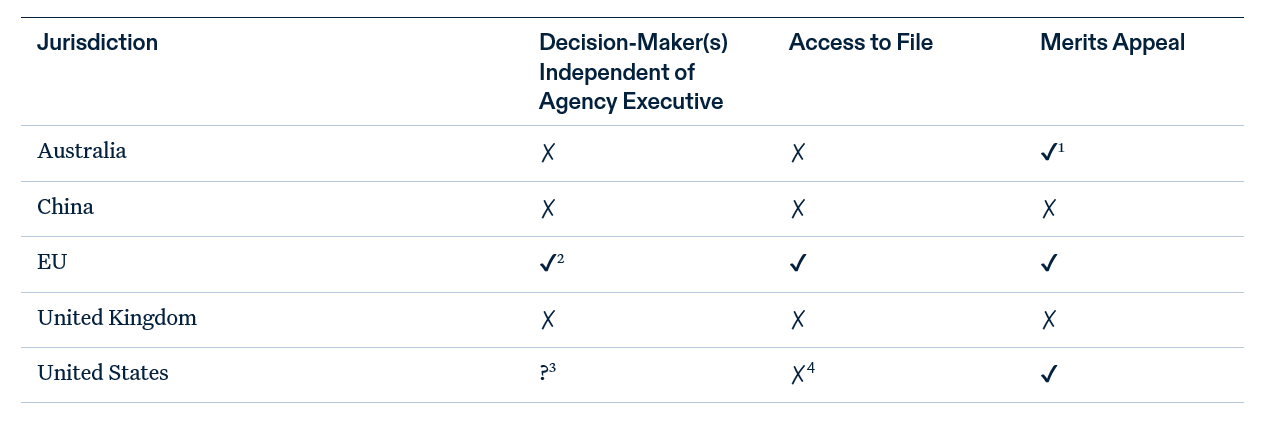

However, the proposal will remove an important “check and balance” on the CMA’s decision-making powers, without any corresponding increase in the appealability of final decisions (such as expanded judicial review or a merits-based assessment like those available in the US or Australia). It will also leave the UK as the only major Western competition regime with a fully administrative merger review process where judicial oversight is limited to judicial review grounds (irrationality, error of law, procedural error), a striking development given the Government’s past use of the panel system as a justification for limiting merits-based appeal rights (including during the merger of the OFT and CC in 2013 and the creation of the Enterprise Act in 2002).

|

|

Tightening Two Key Jurisdictional Tests for Mergers: Share of Supply and Material Influence

-

The CMA has announced it will hardwire further changes into two key jurisdictional tests that lie at the heart of the UK merger regime: the “share of supply” and “material influence” tests. This follows the CMA’s creative application of both thresholds in historical cases, generating significant deal uncertainty and (at times) inconsistent outcomes. The relevance of these tests in the CMA’s reviews also cannot be understated: the share of supply test has acted as the jurisdictional trigger for over three-quarters of Phase 1 merger cases in the last three years. Specific changes include:

-

For the “share of supply” test, the Government plans to tie the CMA’s application of the threshold to six existing criteria in the legislation, namely: (i) value; (ii) cost; (iii) price; (iv) quantity; (v) capacity; and (vi) the number of workers employed – departing from their previous open-ended powers to use any criteria whatsoever.

-

For the “material influence” test, the Government plans to similarly tie the CMA’s application of the threshold to a closed list of four categories of factors, namely: (i) shareholding or voting rights thresholds (e.g., 15%), or shareholding or voting rights in combination with other factors; (ii) board representation or appointment rights; (iii) special voting rights or veto rights over strategic decisions; (iv) confidential strategic information rights; and (iv) commercial, financial or consultancy arrangements. The Government will also retain the power to change these criteria if “new competition challenges arise in the future”.

-

-

While these changes are welcome and have been sought after by practitioners and companies for greater legal certainty, their overall practical impact is likely to be limited. Greater statutory clarity may benefit certain transactions (most notably minority investments), but the CMA’s revised guidance had already narrowed the application of the material influence test last year. The CMA has also always been able to find a basis for jurisdiction under the Enterprise Act where it identifies a substantive competition concern, and there is little indication that these reforms will change that approach.

Major Reforms to the Markets Regime: Procedure and Remedies

-

The Government also announced significant reforms to “improve the pace, predictability and proportionality of the CMA’s markets work”, acknowledging that while the overall impact has been “positive” for UK consumers and the economy (e.g., the open banking regulations or road fuel finder scheme), the end-to-end process can take “over three years”, resulting in delayed benefits to consumers, increased costs and reduced investment and innovation.

-

To address these issues, the Government plans to collapse the existing two-stage regime into a “single-phase market review tool” lasting approximately 6 to 12 months, culminating with either a final report containing the CMA’s recommendations or a consultation process on potential remedies. The CMA will then publish a final report within 6 to 12 months depending on the intrusiveness of remedies being considered, with a single test of “adverse effect on consumers” being used when assessing opening a review.

-

Further, the Government plans to introduce a single test for the markets regime, which will investigate whether there is an adverse effect on consumers. This is the current test for a market study. A full market investigation reviews whether features of the market have an adverse effect on competition. The proposal to move to a test focused on consumers is based on the duty on the CMA to promote competition for the benefit of consumers. The Government considers there may be occasions when the causal link between an adverse effect on competition and identified consumer harm may not be clear – but “the consumer harm is nonetheless material and, if unaddressed, would be liable to damage trust or fairness in markets, and thereby jeopardise their effective operation”.

-

In recognition of the ongoing burden of market enforcement action, the Government will also introduce more regular reviews for market remedies at least once every ten years, as well as a revived commitment to use “sunset clauses” (i.e., where remedies fall away after a set period) by default. Sectoral regulators with concurrent competition powers (e.g., Ofcom, Ofgem, FCA, etc.) will also be able to request that the CMA initiates a new single-phase review, and oversee market remedies imposed by the CMA post-review.

-

It is clear from this scale of the proposed markets reforms that the Government has heard loud and clear from businesses that the burden of long-running market reviews and investigations is too great – even with the welcome procedural changes proposed in the CMA’s revised guidance last year. In the current growth-forward environment, these changes find a better balance between recognising the value of the UK’s markets regime and limiting the burden placed on scarce resources of businesses involved – not just during investigations but also after remedies are imposed.

-

The proposed change of test to a consumer focus is notable. It could enable the CMA to use its considerable remedy powers under the markets regime in circumstances where not only is there no illegal conduct but also there is no identified harm to competition. Under the existing competition-focused test for market investigations, the CMA already has extensive discretion as to features of a market which result in an adverse effect on competition and how to remedy this, including to address any resulting detrimental effect on consumers. Consumer harm – defined as higher prices, lower quality, less choice or less innovation – therefore already feeds into remedy design. Remedies are shaped by the general requirements that they must be as comprehensive a solution to the issue identified as is reasonable and practicable, and must therefore be both effective and proportionate. The CMA (and its predecessor bodies) can go so far as to break businesses up (as occurred in 2011 with the break-up of the former BAA airports) or restructure a market (e.g., by removing vertical integration, as happened in 2005 with BT splitting off its wholesale OpenReach business or, further back, via a 1989 order requiring brewers to end beer supply ties and ownership of pubs). Without the requirement to find that a feature of the market causes harm to overall conditions of competition, just harm to consumers, these wide-ranging powers would be all the more potent and unlimited. The change to a focus on harm to consumers could therefore potentially open up more intervention by the CMA, significantly out of line with the general thrust of these reform proposals (and the CMA’s wider 4Ps initiative) to reduce it.

Other changes: Phase 1 Remedies, Cross-Cutting and the Holiday Period

-

The CMA also announced other changes to the UK competition regime as part of its white paper.

-

Phase 1 Merger Remedies. The CMA will extend the period of time in which Phase 1 remedies can be agreed from 10 working days to up to 20 working days to increase the chances of avoiding a Phase 2 investigation and reduce the burden on merging parties.

-

Other Cross-Cutting Changes: The CMA will be granted powers to demand access to algorithms operated by a company and information on algorithmic behaviour through the issuance of formal information notices. The Secretary of State will also be provided a formal role in a wider range of key CMA guidance documents in line with the requirement for consultation on digital markets, civil penalties and international cooperation guidance.

-

Excluding Holiday Period from Statutory Time Limits: Finally, the CMA also plans to carve out the end-of-year holiday period from merger and markets statutory time-limits in line with some other international merger regimes (like in the EU).

-

* * *